Defined benefit pensions in the UK set a defined benefit at the date of leaving the scheme. This benefit is based on the final salary of the employee and the length of service that they performed with the scheme. Over time the level of benefit grows with UK inflation and is generally linked to either RPI or CPI. The benefits ususally grow both prior to retirement and in retirement. The reason for this is to guarantee the member an inflation adjusted income into the future.

A member of such a scheme may choose to transfer out of such a scheme and in transferring out loses their guaranteed income and accepts market risk in the value of their pension from that point onwards.

If the member transfers out of their UK pension into a New Zealand QROPS and they have been in New Zealand longer than four years then they have to use the schedule method to calculate the tax on their transfer. The schedule method broadly follows the FIF rules and the fair dividend regime. Essentially, this says that the members returns are 5% a year.

The IRD state that no other basis is available for calculating tax on these transfers.

So looking back at CPI inflation in the UK since 1994 the first observation is that not one year has inflation been over 5% (this is even taking into account years that VAT in the UK increased by 2.5% gross on goods).

This automatically penalises an individual as they are paying tax on an assumed 5% growth when every historic data point simply shows this not to be the case.

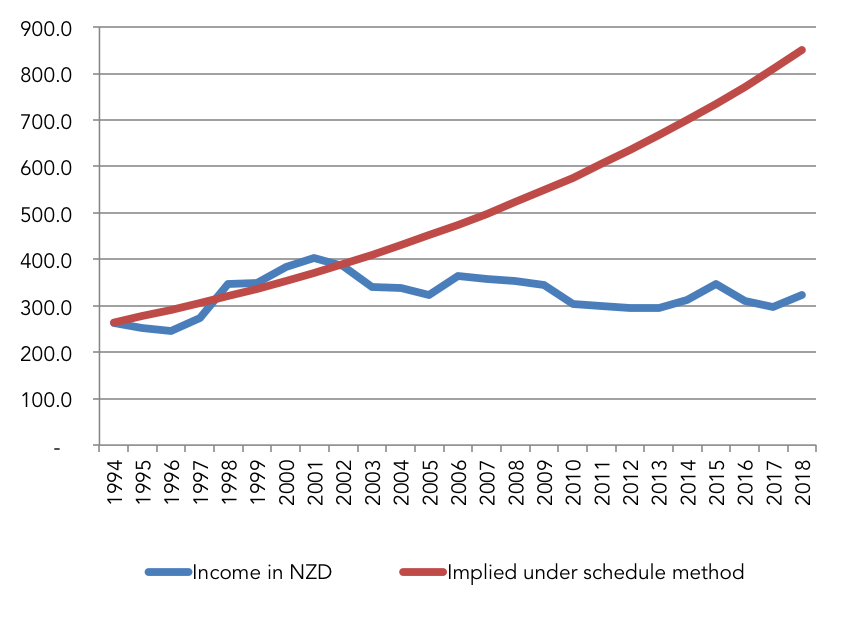

What’s more when consideration is given to the exchange rate effects over that same period (using the average annual GBP:NZD cross rate) you can see that some with an income equivalent of $263.9 a year in 1994 would have seen that income in NZ dollar terms grow to $322.3 in 2018. So over the 24 years that is an increase in income of only 22.1%. Taking the same income in 1994 of $263.9 and multiplying it by 5% a year would imply an income of $874.4 or roughly $610 more that the stating figure. This second figure is what the IRD are effectively saying is the taxable gain. However, the reality for this individual is that they are only actually $60 a year better off.

| Year | Annual CPI Rate % | Inflation adjusted income (GBP100 starting) | Exchange rate NZD:GBP | NZD income |

| 1994 | 2.2 | 102.2 | 2.582 | 263.9 |

| 1995 | 2.7 | 105.0 | 2.404 | 252.3 |

| 1996 | 2.9 | 108.0 | 2.269 | 245.0 |

| 1997 | 2.2 | 110.4 | 2.480 | 273.7 |

| 1998 | 1.8 | 112.4 | 3.093 | 347.5 |

| 1999 | 1.7 | 114.3 | 3.055 | 349.2 |

| 2000 | 1.2 | 115.6 | 3.322 | 384.1 |

| 2001 | 1.6 | 117.5 | 3.422 | 402.1 |

| 2002 | 1.5 | 119.3 | 3.238 | 386.2 |

| 2003 | 1.4 | 120.9 | 2.810 | 339.9 |

| 2004 | 1.4 | 122.6 | 2.761 | 338.6 |

| 2005 | 2.1 | 125.2 | 2.582 | 323.3 |

| 2006 | 2.5 | 128.3 | 2.839 | 364.3 |

| 2007 | 2.4 | 131.4 | 2.721 | 357.5 |

| 2008 | 3.5 | 136.0 | 2.606 | 354.4 |

| 2009 | 2.0 | 138.7 | 2.484 | 344.5 |

| 2010 | 2.5 | 142.2 | 2.142 | 304.6 |

| 2011 | 3.8 | 147.6 | 2.027 | 299.2 |

| 2012 | 2.6 | 151.4 | 1.956 | 296.3 |

| 2013 | 2.3 | 154.9 | 1.908 | 295.5 |

| 2014 | 1.5 | 157.2 | 1.984 | 312.0 |

| 2015 | 0.4 | 157.9 | 2.191 | 345.9 |

| 2016 | 1.0 | 159.5 | 1.949 | 310.7 |

| 2017 | 2.6 | 163.6 | 1.813 | 296.7 |

| 2018 | 2.3 | 167.4 | 1.925 | 322.3 |

The discrepancy is better grapically illustrated below, which shows since 2001 there has been a large divergence between the implied financial gains under the IRD model and the actual benefit gains that have accrued to members.

With such a large difference we simply do not believe that the schedule method is appropriate for the determination of New Zealand tax on transfer for defined benefit schemes.

When looking at the data on a year by year basis there are no periods since 1994 when the inflation and currency adjusted performance would out perform the implied 5% a year return under the schedule method, if a client were to be transferring now.

There are techniques that can be used if you have a defined benefit scheme and are worried about the tax consequences of transferring to New Zealand. These require specialist tax advice and we recommend you contact us to discuss it.