For many considering transferring their UK defined benefit (DB) (aka final salary) pensions, recent declines in transfer values may be concerning. However, rather than waiting for potential increases in your UK transfer value before transferring to a New Zealand QROPS, a strategic transfer approach can help you now. With smart planning you can lower your tax bill, mitigate future risks associated with UK pension regulations and get the same gains if UK DB pension transfer values bounce back.

Step 1 is understanding what really drives final salary transfer values – spoiler its bond yields

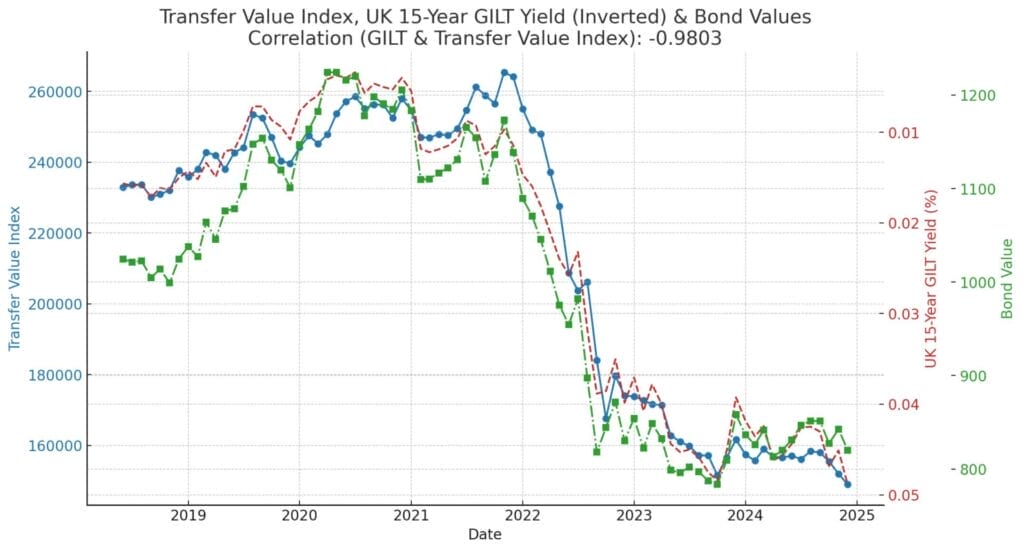

UK defined benefit pension transfer values have historically moved inversely to gilt yields. Over the past few years, rising gilt yields have driven pension transfer values lower. The strong relationship can be seen in the graph below. So if you’re waiting for your transfer value to increase you are essentially waiting for bond yields in the UK to fall. How likely is this to happen – who knows.

So while it’s tempting to wait for transfer values to recover – which means waiting for gilt yields to drop – this comes with its own risks. Specifically the risks are:

- Future UK Regulations: The UK government continues to impose further restrictions on overseas pension transfers already in 2015 they eliminated the ability to transfer out of 40% of all defined benefit schemes in the UK

- More UK Taxes: Any dramatic increase in pension values may trigger additional tax liabilities if you go above the Overseas Transfer Allowance (OTA).

- DB Scheme Failure Risk: Meaning that the company that sponsors the scheme goes bankrupt (like BHS)

- Over Exposure to UK GILTs: UK DB pensions use Liability Driven Investment (LDI) strategies, a gilt crisis in 2022 led to a Bank of England bail out for them. Since then they have increased their LDI exposure putting them more at risk.

There are benefits to UK DB schemes, such as guaranteed incomes and an underwrite from the UK Pension Protection Fund, but this article is focusing on a pension transfer timing only perspective.

Step 2: Mitigate the risks and give you the same upside as a final salary pension value increase

A transfer to New Zealand mitigates risks by locking off UK legislative changes and ringfencing the value of the transferred funds for tax purposes.

Furthermore, if you are waiting for your transfer value to increase you can simply invest the transfer proceeds in a well-structuredbond fund. The key to ensuring long-term value is selecting an investment strategy that provides comparable movements (growth and decline) to UK pension transfer values – see below for an example of how a simple UK GILT index tracker fund has mirrored the performance of UK DB scheme pension transfer values (and GILT yields).

Investing in a bond fund can achieve this and more, and gives you:

- Interest Rate Sensitivity: Bond funds benefit when interest rates fall, which is the same factor that drives up UK pension transfer values.

- Compounded Returns: Rather than waiting for uncertain increases in UK pension values, a bond fund provides consistent growth with reinvested returns.

- Liquidity and Control: Unlike a UK DB scheme, a bond fund gives you access to your money as needed, with the ability to adjust your investment strategy over time.

As with any important financial decision we strongly recommend that you get full financial advice as well as tax advice. Please do not hesitate to contact us about any part of this article.