The first thing to understand is that New Zealand adopts a very different tax regime on superannuation than the United Kingdom – in fact the tax treatment is almost completely the opposite. The differences in the tax regimes can be best summarised in the table below:

| Country | Contributions into the scheme | Growth in the scheme | Payments out of the scheme |

|---|---|---|---|

| New Zealand | Taxed (there is no tax relief on payments into a superannuation scheme) | Taxed (investment gains are taxed in line with personal tax rates) | Exempt (no tax is payable payments out of the scheme) |

| United Kingdom | Exempt (contributions receive tax relief) | Exempt (no tax on the investment gains) | Taxed (payments from the scheme are taxed) |

Payments from NZ QROPS are NZ tax free but could attract UK tax

Distributions from New Zealand superannuation schemes are tax free as they are considered capital distributions rather than income payments. This means New Zealand based members receiving funds from their New Zealand QROPS do not need to declare anything in their New Zealand tax return.

The easiest way to think about New Zealand superannuation schemes is like a bank account – you don’t pay any tax when you take your money out (because the money goes into the account after tax).

The UK has many rules that can lead to taxation on payments from New Zealand QROPS, including:

- Member payment charges of up to 55% – which are charges that are levied on any unauthorised payments made to members from NZ QROPS

- Temporary non-residence income taxes – where the member is considered to have not left the UK for long enough to avoid UK taxes on the payments out of the scheme

Tax is an extremely important area to understand in respect of New Zealand QROPS and we recommend that you get full tax advice before both transferring to a New Zealand QROPS and taking any payments from a New Zealand QROPS.

Tax on investments in NZ QROPS

Any investor that has funds invested in a NZ QROPS needs to understand what part of the growth of their investments will be taxed and at what tax rate. Broadly speaking the tax on your investment growth within your superannuation scheme should mirror the tax that you would pay if you held the investment directly.

The four key factors are:

- Whether you are a transitional resident (or non-tax resident)

- If your a New Zealand tax resident what level of earnings you have

- Whether your investments will be held in offshore funds and assets or in New Zealand funds and assets

- Are the investments going to be denominated in foreign currency

Each of these points requires careful consideration, which we individually explore below.

Transitional (and non) tax residency – 0% tax on investments

Broadly speaking transitional (and non) tax residents pay no New Zealand tax on foreign investment earnings – this is zero-rated income meaning it has a 0% tax on it.

New Zealand has a class of superannuation schemes known as “zero-rate PIE’s” – these are schemes that allow a transitional (and non) tax resident to elect to have a 0% tax rate on the growth in the investments for the period of transitional (or non) residency. This means that for transitional (and non) tax resident their funds can grow free of New Zealand tax during that period. To get a zero-rate status the scheme must hold the majority of its investments in offshore assets – like overseas funds, shares, bonds etc – and the investments in the scheme must be unitised funds run by the scheme itself. Where a scheme invests more than 5% of its funds in New Zealand based investments (shares, bonds etc) it will not be able to be a zero-rate scheme. A zero-rate scheme must apply to the Inland Revenue in New Zealand for it’s status, it is not automatic just because of the schemes investment portfolio.

If you have been in New Zealand for less than four years (having previously not lived in New Zealand for the ten years prior) or are an overseas investor considering a New Zealand QROPS you need to understand the implications of a zero-rate tax environment. We recommend that you talk to specialist about this.

A New Zealand tax resident – investment tax matched to your income levels

A New Zealand tax resident (who is not transitional) can invest in a New Zealand superannuation scheme that allows members to match their investment tax rate to their personal income levels. These schemes are commonly known as PIEs (Portfolio Investment Entities) and require that you work out your rate of tax on investment growth which can either be 10.5%, 17.5% or 28% depending on your income levels. The lower the income the lower the tax rate – see the Inland Revenue guidance here. PIE schemes suit those on lower income as they will end up paying less tax.

Where a New Zealand superannuation scheme is not a PIE the 28% rate of tax will be applied to investment growth on the funds. The non-PIE schemes tend to have a lot wider offering of investments and suit those who would be on a 28% tax rate regardless.

It is important to get your tax rate on the growth correct and choose a scheme type that can help minimise your tax obligation. We recommend that you speak to a professional adviser to do this.

Foreign investments and the tax rules

A foreign investment is one that is held outside of New Zealand. For the purposes of clarification, a sterling bank account held with HSBC NZ for example, is not a foreign investment as the account is effectively held in New Zealand.

It is important to understand the distinction between foreign held investments and domestic investments as it affects the tax treatment. Truly foreign held investments, such as overseas bonds, unit trusts etc, fall under the Foreign Investment Fund (FIF) rules.

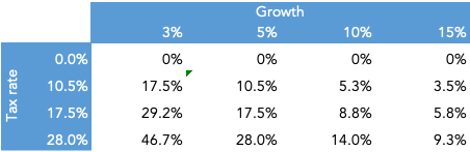

Under the FIF rules the investment is assumed to grow at 5% a year and the investor pays tax on this assumed 5% growth. If the assets are growing at greater than 5% a year the investor has a tax advantage any growth less than 5% and the investor is tax disadvantaged. This is demonstrated in the table below that shows the different effective tax rates for an investor depending on their NZ investment tax rate and the growth rate in the fund.

Domestic investments and the tax rules

Where the investments are domestic the same tax rules apply to the growth in the investments as if the member of the superannuation scheme had made the investment themselves. That means no tax on capital gains in New Zealand. Again this can mean the effective tax rate on the investments is low where the majority of the investment gains come through capital gains.

| 5 year gross | After tax at 28% | Actual effective tax rate | |

| Growth fund | 11.79% | 10.90% | 7.5% |

| Global Equity | 12.78% | 12.07% | 5.6% |

| Income fund | 7.79% | 6.22% | 20.2% |