Initial fees – transfer and entry fees

Initial QROPS fees are fees related to getting into a QROPS in New Zealand and your funds ready to be invested. The fees in the table below are indicative and not every scheme charges each fee, but it is important that you understand what you will be charged.

Almost all QROPS in New Zealand do not charge for transferring into their scheme – in essence offering a ‘free transfer service’.

Table 1: Initial fees that might be charged by QROPS and their potential levels

| Fee type | Scheme Entry fees | Adviser fees | Exchange rate fees |

| Comment | QROPS may charge entry fees as either a % of the transfer value or a simple flat fee for becoming a member of the scheme and completing the transfer paperwork. | Getting good advice on a pension transfer is crucial. Usually a QROPS will allow you to charge the advisers fees against your pension funds when the transfer arrives. If the QROPS doesn’t allow you to recharge your adviser fees you may need to pay these directly. | Most pension transfers arrive in GBP. At some point you might convert your funds to New Zealand dollars. It is important to understand what exchange rate the QROPS will offer. |

| Amount of transferred value | Range 0% – 1% Usually 0% | Range 0% – 5% Agreed between member and adviser | Range 0.1% – 2% Usually 0.14% |

| Charged by | The QROPS | The adviser – paid either through the QROPS or directly by the client | The bank and/or the QROPS |

Source: Our analysis of NZ schemes product disclosure statements and annual accounts

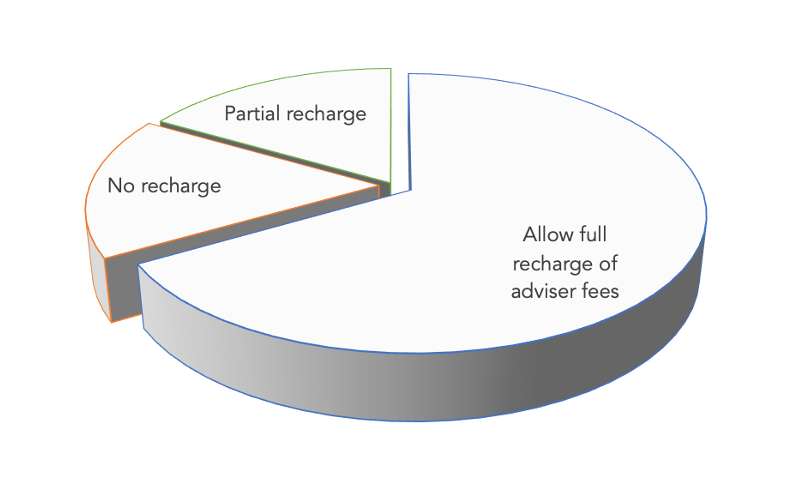

The majority of QROPS also appreciate that getting good advice on a pension transfer is imperative. As the rules allow QROPS to pay advice fees out of members funds without penalty most QROPS offer this valuable service to their members (otherwise the member might end up having to pay the fees directly and not being able to access the funds in the scheme to subsequently compensate themselves). As can be seen in Figure 1 below the majority of NZ QROPS offer the ability for members to pay their professional advisers directly through the funds in the scheme.

Figure 1: QROPS that allow adviser fee recharge

Source: Our analysis of NZ schemes product disclosure statements and annual accounts

Ongoing fees – Scheme operation fees

There are many ongoing fees within superannuation schemes in New Zealand relating to the operation of the scheme and the management of the funds that members invest in.

Table 2: Scheme operation fees that might be charged by QROPS and their potential levels

| Fees | Comments | |

| Annual scheme management fees | These are the fees that are paid to the manager of the scheme to run the scheme. They are often slightly higher than normal superannuation scheme fees. The reason for this is because there are both New Zealand and UK reporting requirements for QROPS. The fees are typically around 1% a year. | |

| Trustee and audit fees | These fees are usually paid out of the annual scheme management fees, although some scheme choose to separate them out. It is important to understand what is included in the scheme management fees. |

Our review of the New Zealand based QROPS product disclosure statements

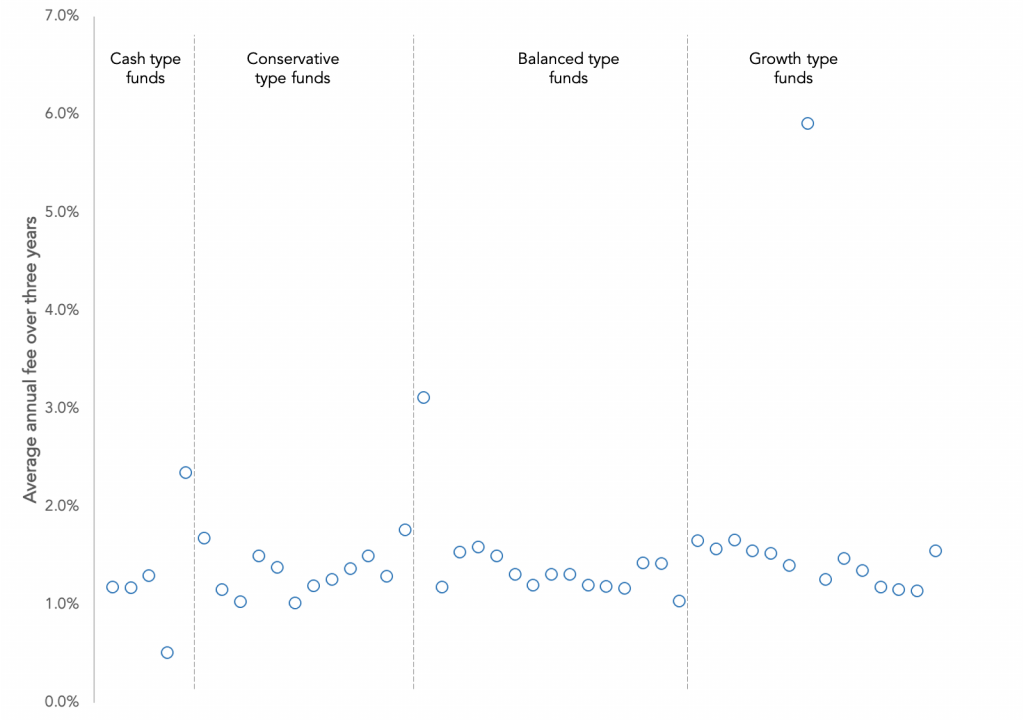

Small differences in fees can make big differences in your long term performance. Our analysis shows that there is variability in fees charged across funds run by New Zealand QROPS schemes as shown in figure 2 below. When we looked at the average annual fees charged over the last three years some funds fees were driven up by the payment of performance fees getting to nearly 6% a year. Most funds did not charge performance fees.

Figure 2: Average annual fees (over the last three years) by funds within fund types

Source: Our analysis of NZ schemes fund fact sheets

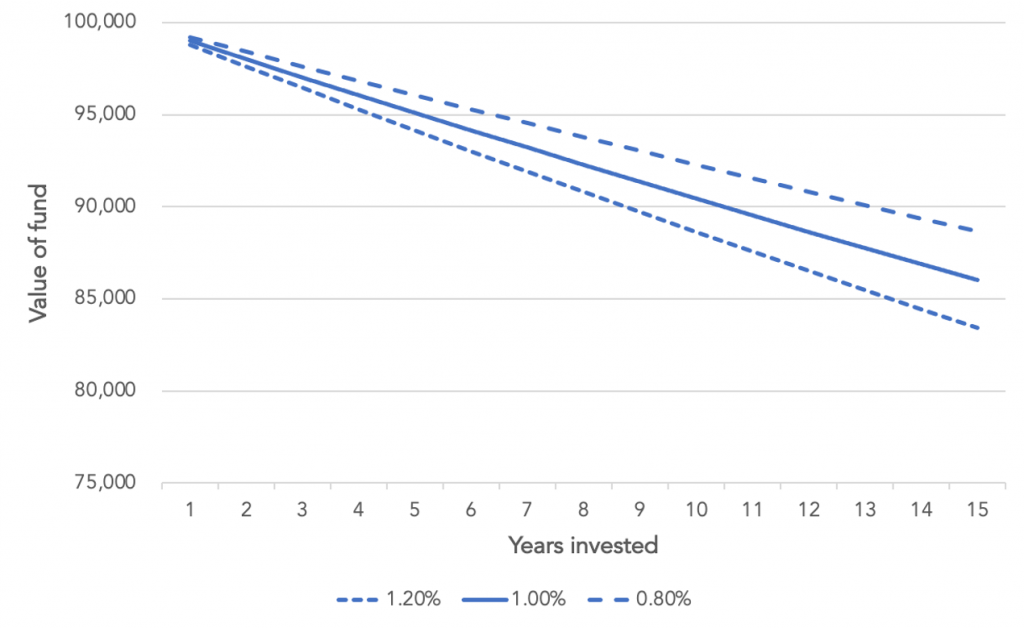

We also observed that the ‘estimate fees’ quoted in the product disclosure statements can sometimes vary significantly from the actual fees charged on the funds. It is very important that you get expert financial advice when choosing funds as fees can play a big role in your final returns. the table below shows how a 0.2% fee difference a year can make a $2,500 difference on $100,000 investment over 15 years.

Figure 3: How small differences in fees can make differences on your fund value in the long term

Ongoing fees – fund fees

Once you have your money in a QROPS in New Zealand it needs to be invested in funds. These funds will give differing returns and have have different risk profiles. Similarly they will have different fees associated and attached to them, some schemes charge to switch between funds, some funds have entry and exit fees, some charge performance fees. There is a wide spectrum of costs and you need to be aware of all of them when investing. We recommend that you speak to a professional adviser so that you can see what all the underlying costs will be.

Table 3: Fund fees that might be charged by QROPS and their potential levels

| Fee | Comments |

| Fund management fees | These are fees paid to the underlying fund manager for investing your money in their funds. These fees can range from low cost EFT fees to higher cost management and performance fees. Usually the fees range between 0.3% and 0.7% although we have seen them as higher as 2% – 3% or more. The important things to check for in fund management fees are: – Whether any of these fees are rebated to the QROPS – Whether any of the fees are rebated to the adviser who recommended the funds The above points must be disclosed by all parties. |

| Fund platform fees | Investment platform schemes sit on top of fund platforms. These platform run the investment and custodian services, as well as calculating the tax on the growth in the funds. For this they charge fees. The fees are usually based on a clients balance and usually range between 0.35% and 0.6% depending on the platform chosen and the amount of funds invested. |

| Fund entry and exit fees | Some funds charge a fee for investing into their funds as well as selling out of them. These fund fees might be up to 2.5% and so moving between funds can be very expensive. |

| Fund switching fees | These are often charged at the scheme level and are a fee for the administration involved in switching between funds. |

Exit fees – withdrawing funds or leaving a scheme

Some schemes charge a fee for exiting the scheme, this can come in one of two forms:

- Withdrawing your funds from the scheme within a specified period (say 24 months)

- Transferring out of the scheme

It is important to understand if your scheme intends to charge these fees.