Reforms in the UK start the ball rolling

UK pensions have been transferred to New Zealand since the 1990’s, and it was a relatively cottage industry back then. The advent of Qualifying Recognised Overseas Pension Scheme (QROPS) regulations in the UK in 2006 changed that somewhat as it made the process of transferring out of a UK pension scheme easier and more ubiquitous as well as giving New Zealand schemes some rough guidelines to follow.

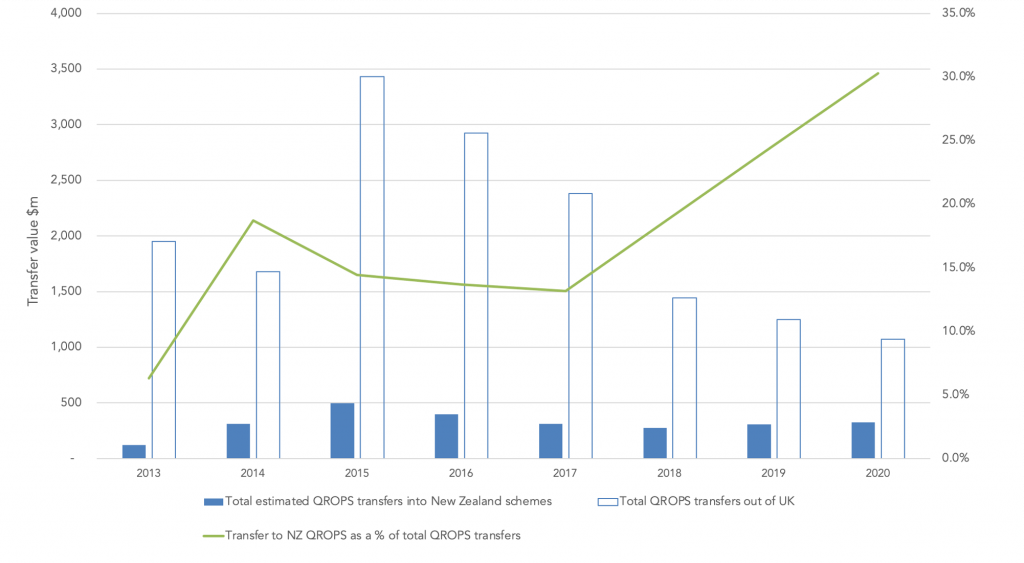

What started as a trickle of transfers out of the UK in 2006 soon grew to a billion pound annual industry, culminating in 2015. Once the genie was let out of the bottle by the HMRC they have been trying to put it back with a series of measures to reduce transfers overseas, the largest of these has been:

- Stopping transfers out of public sector pension schemes in 2015

- Introducing an overseas transfer charge (OTC) of 25% for transfers to a scheme that is not based in the country of the transferee

The cumulative impact of these has seen pension transfers drop to around a third of their level in 2015.

Figure 1: HMRC figures on transfers out of UK schemes to QROPS

Source: HMRC

New Zealand QROPS market development

The New Zealand always featured as the best destination for a UK pension transfer because of its favourable tax regime, but it previously lagged behind in investment options and sophistication. This has been a blessing, as New Zealand QROPS have not developed high fee portfolio bonds like those seen in Malta and Gibraltar. Instead they have set to develop fully transparent fund offerings where clients have access to reputable fund managers, with full visibility of all fees and returns.

The New Zealand QROPS industry has developed investment diversity quickly with most QROPS now offering sterling, New Zealand dollar and Australian dollar denominated funds. The sterling funds have certainly been popular with most transferees since the Brexit vote, especially as there is more control over when they can be converted into dollar funds. This level of control and flexibility is in sharp contrast to the previous system of waiting for the desired exchange rate then starting a transfer which then took six months by which time the exchange rate was anyone’s guess.

Figure 2: NZ QROPS transfers versus total QROPS transfers

Source: Annual reports of New Zealand superannuation schemes that are listed as QROPS and HMRC data.

Investment options have developed in New Zealand QROPS

New Zealand can be attractive for UK pension transfers because of the tax regime, for both residents and non-residents, but in the past the number of schemes and the investment options were more limited.

The New Zealand QROPS industry has developed investment diversity quickly with most QROPS now offering sterling, New Zealand dollar and Australian dollar denominated funds.

Figure 3: Fund currency split among NZ QROPS

Source: QROPS product disclosure statements 2021

Figure 4: Single currency schemes versus multi-currency schemes

Source: QROPS product disclosure statements 2021